For foreigners who are purchasing Thai property, they have to pay for the purchase with any currency other than Thai baht. Without getting too technical, there is a rule in Thailand that states that for foreigners, foreign currency has to be used in the purchase of Thai properties. On top of that, the payment has to be done within the international banking system. This means that the foreign currency needs to be transferred from a foreign bank to a Thai bank.

Let us consider this example: A Malaysian would like to purchase a THB 7 million condominium in Bangkok

There is a 30% downpayment for the condominium.

The Malaysian would need to pay THB 2.1 million for the condominium to Bangkok. However, he cannot make this payment in baht but rather, he has to make this payment in a foreign currency. His obvious currency of choice would be the Malaysian ringgit.

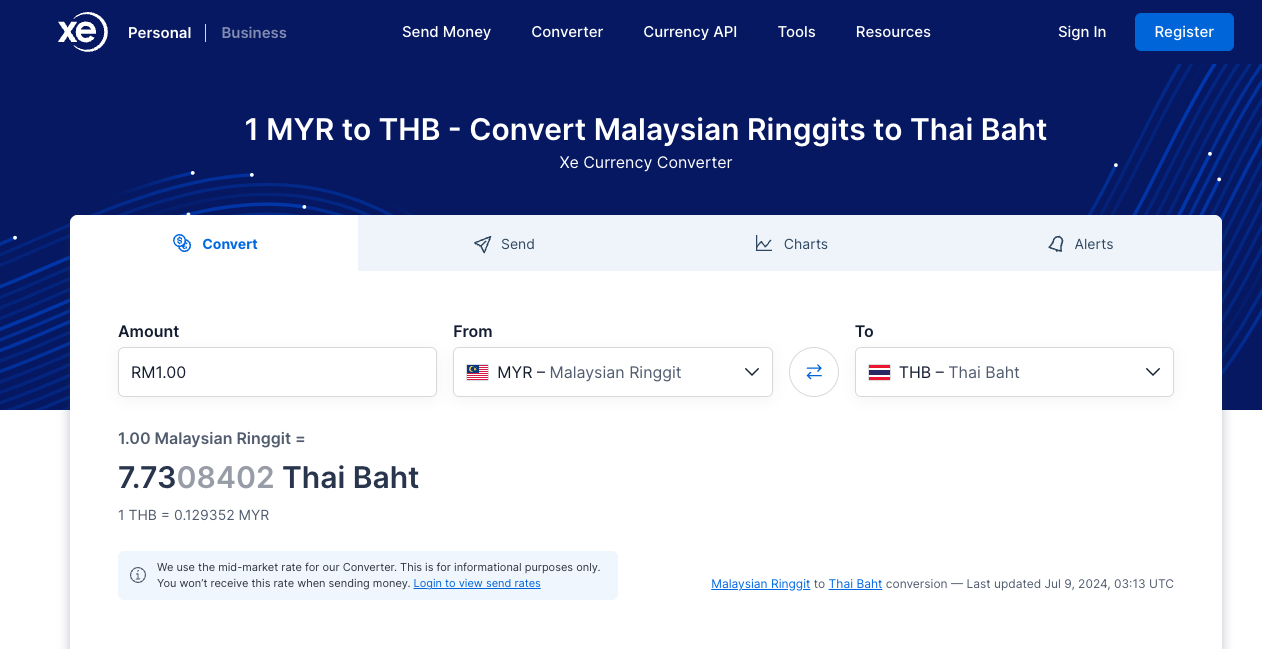

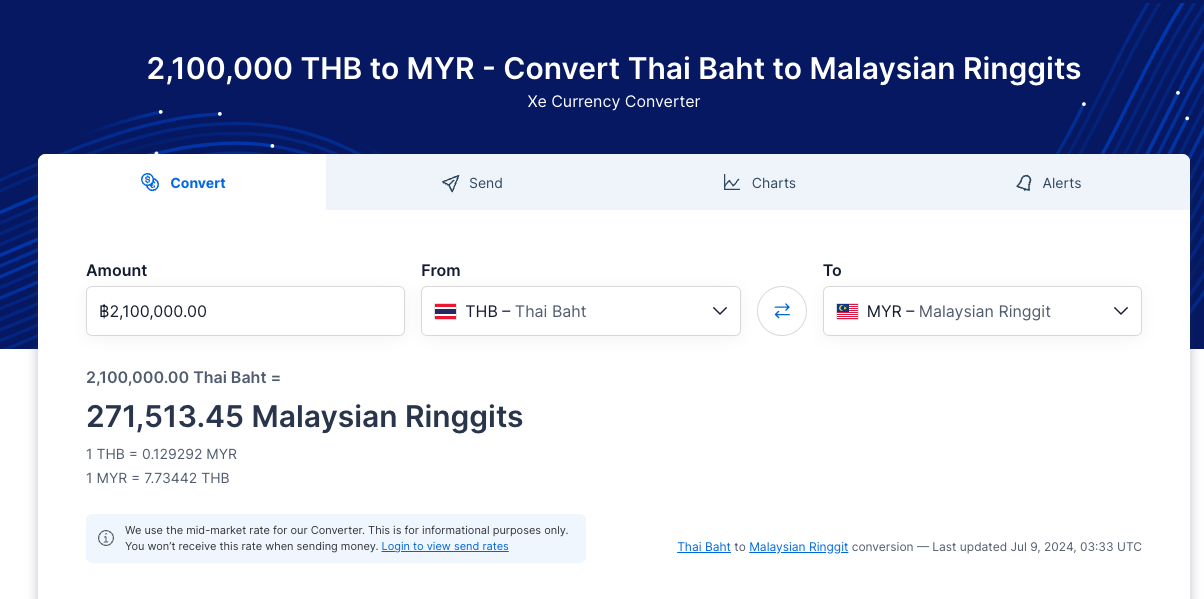

So he goes on to a currency conversion site like XE currency and checks the exchange rate and this is what he sees.

As of 9th July 2024, the exchange rate is 1 Malaysian ringgit to 7.73 Thai baht. If he wants to transfer THB 2.1 million exactly, he would need to transfer 271,513.45 ringgit to the developer’s Thai bank account.

However, this is the rate that XE Currency is offering. When the ringgit reaches the developer’s Thai bank, it will be converted based on the rate at the Thai bank. This rate can be higher or lower than XE currency. Moreover, the money will only reach the developer’s Thai bank in perhaps a day or two. The rate would be different. There is also the issue of bank charges for the telegraphic transfer. In short, it is close to impossible for him to make a transfer that will equate to the developer receiving exactly THB2,100,000. Since the developer requires exactly THB 2,100,000 and no less, the only option would be to transfer a bit more. The issue is how much more?

The Malaysian would know the bank charges on his end, i.e. his Malaysian bank. However, he may not know the bank charges over at the developer’s end. Yes, the bank charges can be found on the bank’s website but different types of accounts may have different charges for telegraphic transfers. Therefore, the prudent thing to do in my opinion would be to buffer for 5% more. In this case, I would advise the Malaysian purchaser to transfer at least 105% x 271,513.45 = 285,089.12 ringgit. In fact, I would round it up to the nearest thousand and advise that he transfer 286,000 ringgit.

The question that results from this would be, “How then are excess monies paid accounted for”?

The answer to that would be that excess monies can be rolled over to the next time the purchaser needs to make another payment. In this case, when the condominium is completed, the developer will require the purchaser to make the final 70% payment of the THB 7 million. The purchaser can offset the previous excess payments in this payment. However, I would still recommend that the purchaser makes the transfer without considering the previous excess payment. The excess payments can be consolidated and then returned to the purchaser when he or she collects the keys to the property. This is in the form of a cheque which can then be banked into a Thai bank account.

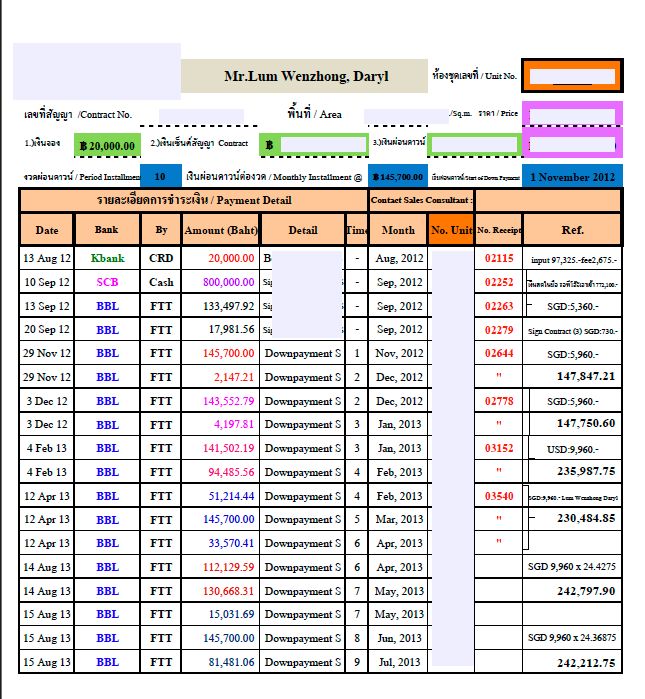

At every stage of the transfer, the developer will provide an update in table form as to how much money has been paid. Therefore, there will be a record as to the excess monies that were transferred.

This is an example using a property I purchased. It was some time ago and hence the payment schedule for this development consisted of quite several transfers. I thought that this would be a good illustration of how organised the schedule provided by a developer is. Do note that the payment schedule these days is a lot less complex. It is usually two transfers of 15% with one final transfer of 70%.

The table above was sent to me via email every time I made a transfer. From there I could tally the excess payments I made and eventually, the developer returned the excess amount to me in the form of a cheque. I banked it into a Bangkok Bank account. I opened that bank account using the sales and purchase agreement of the condominium. This is what happens when foreigners purchase a condominium from Thailand.

I cannot say that this is the norm for all property developers. However, I have dealt with just about all major property developers in Bangkok and this is how they deal with all foreign purchasers and money transfers. This is the reason why I have always reiterated that foreign buyers should be making Thai property purchasers from established developers. The process is well settled and communication is extremely organised and easy to understand.

Yours sincerely,

Daryl